[ad_1]

DjelicS

Overview

I stand by my recommendation that Rover Group (NASDAQ:ROVR) is undervalued. Rover is the leading pet services marketplace in the US, Canada, and Europe. Rover is a platform that links pet owners with sitters who can care for their pets both during the day and at night. Increased pet ownership and the humanization of pets are two secular tailwinds that make the pet services market an appealing opportunity. Rover’s size and scope make it the dominant player in its field, giving it an edge over its closest competitor, Wag. An interesting inflection point is upon Rover in FY23 as it is expected to turn breakeven on an EBIT basis, which in my opinion significantly reduces the need to rely on capital markets to pursue growth opportunities. In fact, Rover will have more opportunities to tap into the debt market for international expansion and new service/pet offerings. All in all, I continue to recommend a long position but would cautious investors on near-term stock price volatility in the face of a volatile macro environment.

4Q22 earnings

With a year-over-year increase of 31%, Rover’s reported GBV of $218 million is just slightly higher than consensus forecasts of $214 million. The company’s revenue increased by 37% year-over-year to $52 million, and its EBITDA increased by 46% to $11 million. What I took away from the earnings was that underlying bookings remain very solid, and the combination with a better take rate led to better-than-expected upside. The key parameters and variables for the company’s future operations were also clearly communicated by management. Specifically, management is warning of a slowdown in the first quarter of 23 and an uptick in cancellations throughout the year. However, there was some encouraging news shared by management regarding international growth, new customer acquisition, and repeat bookings. In general, I think that ROVER had a strong fourth quarter showing, which was fueled by the increasing popularity of ABVs and new bookings. Management also confirmed their goals of achieving 20-25% growth in revenue, with a contribution margin of over 80%, and adjusted EBITDA margins of more than 30%.

Guidance

The management team gave guidance for both the first quarter of 2023 and the full fiscal year of 2023. Here are the details:

- For the first quarter of 2023, the GBV (gross booking value) was projected to be $190 million, which represents a decrease of $32 million from the previous guidance. Revenue was projected to be $38 million, with an adjusted EBITDA of -$4 million.

- For the entire fiscal year of 2023, the GBV was projected to be $958 million, which is $39 million less than the previous guidance. Revenue was projected to be $213 million, with an adjusted EBITDA of $28 million.

Financials

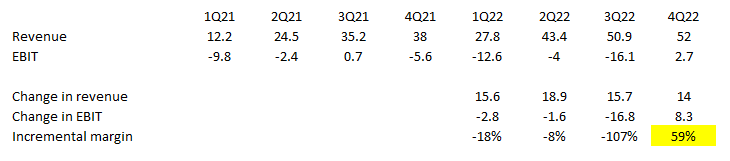

A look at Rover 4Q22 results suggest strong operating leverage that I believe to continue from here on out. Rover EBIT went positive for the first time despite being in investment mode. While the analysis I have provided is not entire accurate, but it points to a strong incremental margin that Rover should continue to print moving forward. At 59% incremental margin, we can expect to see strong EBIT growth.

Own analysis

Given now that we have a visibility into Rover path to achieving long-term margins, we can now, with confidence, back into what multiple Rover should trade at. Based on my math below, assuming Rover trades at a 2x premium to SPX forward PE given it is growing faster, and a long-term net margin of 15% based on management EBITDA guidance, it suggests that Rover should trade at 3x forward revenue.

Own analysis

I have updated my model to reflect this multiple, which translates to a 60% upside using consensus estimates in FY26.

Own model

Stock price cadence

The rise in share price following the 4Q results suggests that investors agree with my assessment, and I like the idea of Rover touching positive EBIT grounds. However, as I mentioned above, the 2023 revenue outlook was pretty mixed, particularly in light of the notable slowdown compared to the 1Q revenue guide of 37% growth. This 37% growth, however, is likely attributable to the easier Omicron comp in 1Q, so I’d like to set readers’ expectations appropriately. In addition, I believe management is being cautious by anticipating a mild to moderate recession that grows throughout the year and reaches its peak around midway through the second half of 2023. Given that Rover does not appear to be experiencing any major macro impact at the moment, I believe this estimate to be conservative. Strong profitability and the announced $50 million share buyback program have both contributed to the stock’s positive narrative. As more investors become confident in FY23 numbers, I anticipate a gradual upward trend in the share price through FY23. As we approach the third quarter of FY23, I anticipate that investors will begin looking ahead to FY24, which I believe will be a better environment than the weak and uncertain FY23 we are currently facing. After that point, investors’ risk appetite for growth stocks should increase, which should further support Rover stock price.

How Rover’s marketplace will function in a volatile macroeconomic environment is likely to be the primary topic of debate among investors in the near future. Despite the short-term uncertainty of the macroeconomic environment, I still see Rover as a strategically advantageous two-sided marketplace for online pet care that brings together pet parents and pet care providers across North America and Europe.

Conclusion

I maintain my buy recommendation that ROVR is undervalued and has significant growth potential as a leading pet services marketplace. The strong 4Q22 earnings report with a year-over-year increase of 31% in GBV, and positive EBITDA growth, reinforces my confidence in the company’s future. While there may be some near-term stock price volatility due to a volatile macro environment, I anticipate a gradual upward trend in the share price through FY23 and beyond. Overall, I continue to recommend a long position in ROVR for investors seeking exposure to the growing pet services market.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.