[ad_1]

JacobH

Note: All amounts discussed are in Canadian Dollars, unless specified otherwise

Dodging stocks that completely collapse is becoming harder and harder for investors. While the indices have held up, many smaller companies have got annihilated. Fortunately, many stocks do present glaring red flags that we have been able to use to stay away. Uranium Royalty Corp. (NASDAQ:UROY) (TSXV:URC:CA) was certainly one of them. Almost exactly a year ago, we told people to ditch the euphoria of the Uranium run and head for the exits like The Road Runner. Keep in mind that in the two years leading up to that article UROY had delivered 500% returns.

But an insane valuation made us believe that this was yet another bubble of epic proportions. Since then UROY has wiped off a few smiles and the stock is now down 56% over the last year.

Seeking Alpha

Please note the price in the above graphic is in USD.

We look at the recently released results and analyze whether the flaws we pointed out previously are still present or not.

Q3-2023

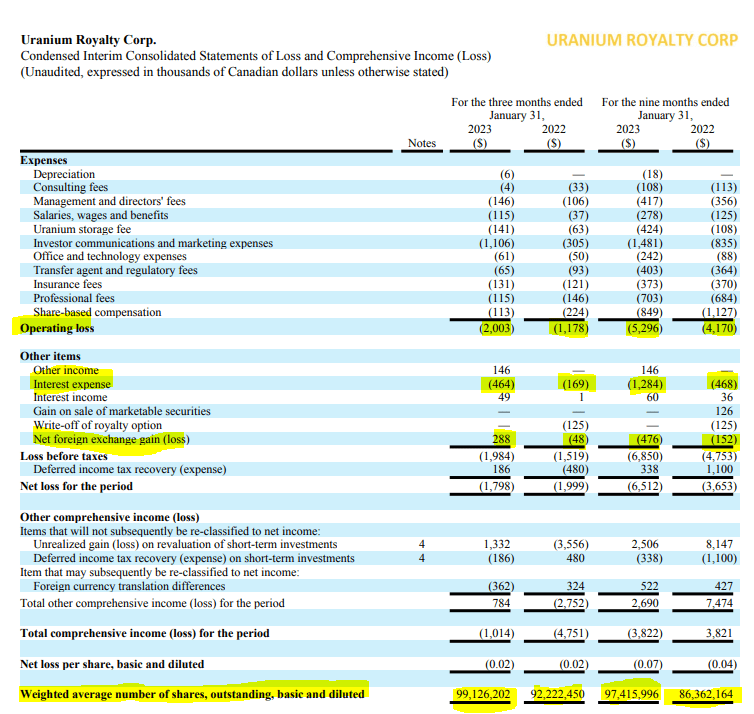

UROY has its fiscal year ending in April. The recently released results for January 31, 2023 were for the third quarter of the current fiscal year. We will go over the income statement and balance sheet and highlight items that investors should pay attention to. For this quarter the operating loss was close to $2.00 million.

UROY Q3-2023 Financials

What should be notable above is the lack of any revenues. We have seen these in a few bubble stocks and occasionally even “negative revenues” can show up. So all you have is the cash drain. You can see this consistently for all 3 quarters of this year and you can see this for last year as well. The operating loss this quarter is actually one of the higher ones as investor communication and marketing expenses took off. Beyond the operating loss, we see that interest expense also moved up sharply. This expense relates to the margin loan facility which is described below.

On May 7, 2021, as amended and restated on January 17, 2023, the Company established a margin loan facility for a maximum amount of approximately $18,552 (US$15 million) (the “Facility”) with the Bank of Montreal. The margin loan is subject to an interest rate of Adjusted Term SOFR Rate plus 5.50% per annum and the unutilized portion of the Facility is subject to a standby fee of 2.50% per annum. The Adjusted Term SOFR Rate shall mean on any date the Term SOFR Reference Rate published by CME Group Benchmark Administration Limited for the tenor comparable to the applicable interest period, plus credit spread adjustment. In addition, the Company paid a one-time facility fee equal to 1.25% of the Facility. The Facility is secured by a pledge of all the ordinary shares of Yellow Cake held by the Company. The Facility matures on May 5, 2023, unless repaid earlier, and is subject to customary margin requirements and share price triggers. The Company may voluntarily repay the outstanding amount during the term of the Facility.

Source: UROY Q3-2023 Financials

This part is a bit confounding to us and we will tell you why when we get to the balance sheet. The next item we have highlighted above is the foreign exchange gain or loss. We are highlighting this one to tell investors to ignore it. In other words, calculate total losses excluding this amount. So total real loss for this quarter would be the operating loss plus the interest expense, or about $2.5 million total.

The final part highlighted is the number of shares outstanding. The weighted average number of shares is higher by about 13 million year over year, or close to 14%. This of course is the only source of funds for the company. Share issuance. Over the last 3 years share counts are up about 40%.

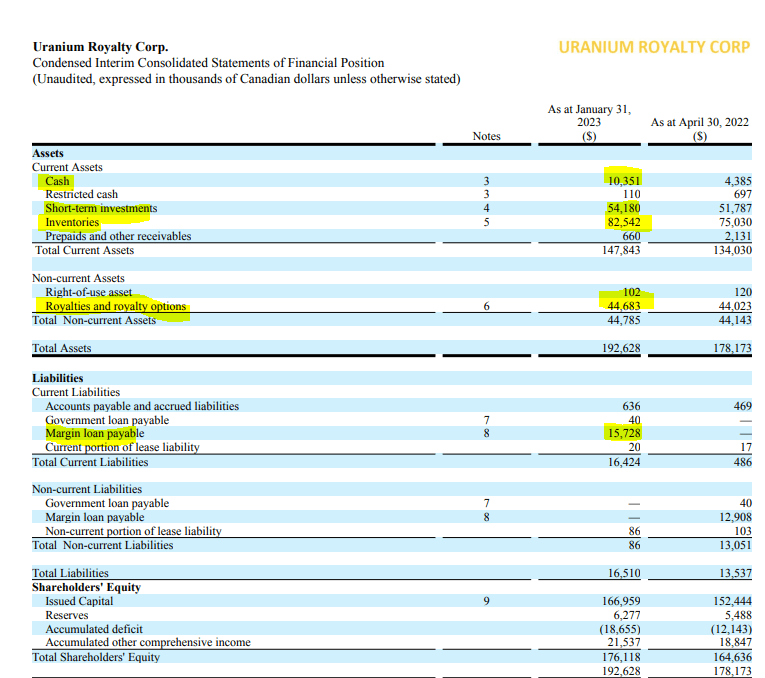

Moving on to the balance sheet, we see that the company has close to $150 million in current assets.

UROY Q3-2023 Financials

This includes $10.35 million in cash, $54.18 million in investments and $82.54 million in uranium inventories. The short term investments is primarily focused in Yellow Cake plc (OTCQX:YLLXF), which is also a Uranium holding corporation. Royalty assets are about $44.6 million which is basically unchanged since last year. The bulk of the change here is due to currency differences impacting valuation. Finally we have the $15.7 loan on which UROY is paying interest. Considering that it has over $10.3 million in cash and zero revenues, we fail to see why this margin loan is maintained. Ideally, the company can issue even more shares to pay that off.

Outlook & Verdict

As we have seen above we have a cash burn rate of about $10 million a year and zero revenues. This is offset to some extent by the tangible assets including uranium investments and royalty assets. At present the total shareholder equity is about $176 million and that works to close to $1.78 per share. Note that we are discussing everything in Canadian dollars. So in US dollars that is about a US$1.29 per share. You might argue that we should pay a premium for royalty assets. Sure, if they were producing some revenues. Currently there is nothing but a solid burn rate offset by new share issuance. Unless the uranium bull market begins in full earnest and the mania comes back, we see that number ($1.29 US) as the best point to wager on the long side. Of course that point is far closer to today than at the highs and valuation is steadily improving. That’s the good news. The bad news is that those that bought at the highs will continue to hurt. We rate this as a hold/neutral at present.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.