[ad_1]

bfk92

ZIM Integrated Shipping (NYSE:ZIM) presented its fourth-quarter earnings sheet yesterday and the company’s results beat both top and bottom line estimates which caused shares to soar 7%. However, the shipping company also expects a large decline in adjusted EBITDA and earnings in FY 2023 as the container industry contends with lower shipping rates and potentially a contraction of shipping volumes in a recession environment. The EBITDA outlook for FY 2023 was also much worse than I expected. Additionally, investors are set to see drastically lower dividend payments this year as leaner times are ahead!

ZIM Integrated Shipping Q4: Everything You Need To Know

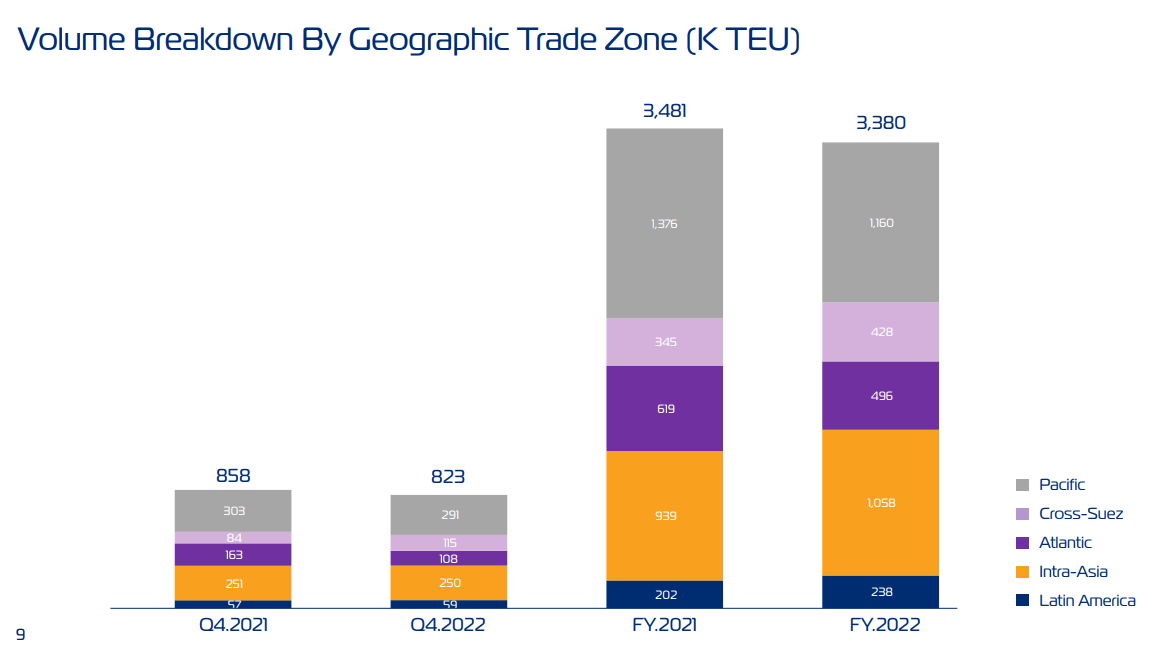

ZIM Integrated Shipping, given the circumstances in the industry, reported decent results for its fourth-quarter, but the trend in key metrics shows that the down-turn in the shipping industry has started to profoundly affect the firm’s fundamentals. Shipping volumes fell 4% in Q4’22 to 823 thousand containers and the company has suffered a steep, but expected decline in freight rates. The decline in freight rates (discussed in the next section) hit the shipping company hard as rates declined 42% in the fourth-quarter to just $2,122/container (average rate). Due to the deterioration of pricing power in the industry throughout FY 2022, ZIM Integrated Shipping’s free cash flow also declined. The firm’s free cash flow crashed 37% to $1.05B compared to the year-earlier period.

Source: ZIM Integrated Shipping

ZIM Integrated Shipping achieved Q4’22 adjusted EBITDA of $973M, showing a decline of 59%. Full-year adjusted EBITDA, however, was $7.54B and showed an increase of 14% compared to FY 2022, but largely due to strong freight rates in the first half of the year. Given the decline in pricing that has occurred in the shipping industry due to faltering consumer demand, especially in the second half, ZIM Integrated is unlikely to repeat this performance in the near or medium term, in my opinion.

Source: ZIM Integrated Shipping

Shipping rates continue to slide

Shipping rates are now longer in complete freefall, but they are still sliding… which is set to continue to put pressure on ZIM Integrated Shipping’s average freight rates, free cash flow and adjusted EBITDA. According to the Drewry World Container Index, shipping costs declined yet again to $1,806 per 40-foot container, as of last Thursday. This price reflected a 3% decline from the previous week and a massive 83% decline compared to September 2021 which is when freight rates topped out at $10,377.

Source: Drewry

Risk to container volumes

ZIM Integrated Shipping’s container volumes have fallen in FY 2022 to 3.38M containers, down 3% from 3.48M containers in FY 2021 with volume declines materializing on Atlantic and Pacific trade routes. Contracting container volumes while shipping rates are falling could further put the screws to the industry, especially if the global economy is pushed into a recession in 2023.

Source: ZIM Integrated Shipping

Outlook for FY 2023 and drastic decline in dividend payments

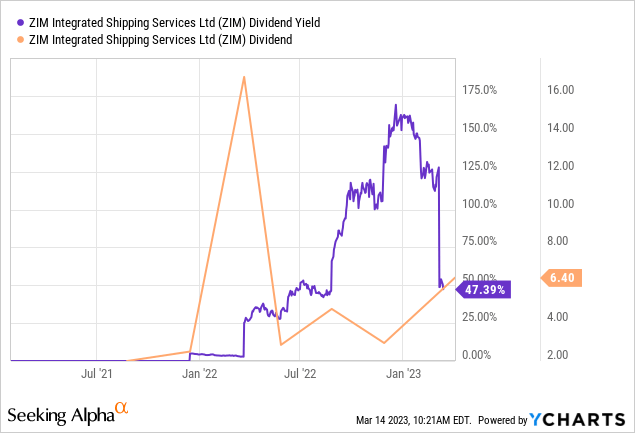

The disappointing part of ZIM Integrated Shipping’s earnings release was the outlook which calls for just $1.8B to $2.2B in adjusted EBITDA in FY 2023. Since ZIM Integrated Shipping reported adjusted EBITDA of $7.54B for FY 2022 — which fell right in the middle of the company’s stated EBITDA guidance of $7.4B to $7.7B — the target for FY 2023 implies a massive 73% year over year decrease in this important key metric. Although ZIM Integrated Shipping is expected to remain profitable this year, investors are set to see a drastic decline in dividend payments as a result.

The company’s appeal in the last few years has been its juicy dividend payout. ZIM Integrated Shipping paid $16.95 in dividends in FY 2022, including a $6.40 per-share dividend in Q4’22 which translated to a 44% net income payout ratio. ZIM Integrated Shipping pays a variable dividend that depends on net income… which, as you will see in the next section, is set to disappear completely next year. I estimate that the shipping company will pay a dividend between $3-4 in FY 2023 to reflect the deterioration in operating conditions, so the fat dividend times of FY 2022 are clearly over for ZIM.

ZIM Integrated Shipping’s valuation

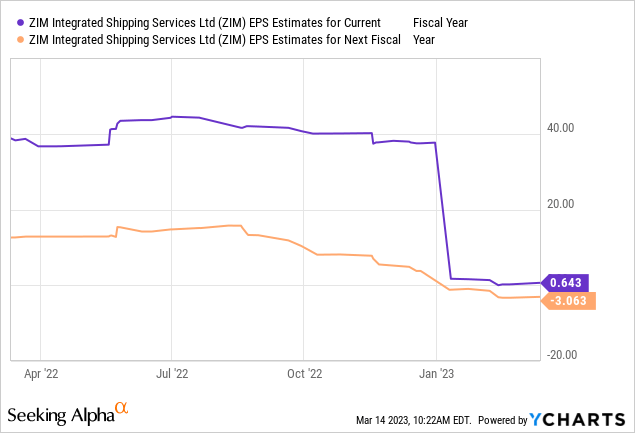

ZIM Integrated Shipping currently has a price-to-earnings ratio (FY 2023) of 32.4 X based off of an average earnings projection of $0.64… which implies that the market continues to expect a continual down-turn in the shipping industry. Additionally, EPS projections for FY 2024 have turned negative which makes the application of a P/E ratio impossible. Given the steep decline in EPS estimates — especially for FY 2023, see below — I believe the risk profile for ZIM remains unattractive.

Risks with ZIM Integrated Shipping

ZIM Integrated Shipping is already facing a significant and severe downturn in the container shipping industry which has resulted in declining free cash flow and EBITDA, and the outlook for FY 2023 clearly shows that conditions are expected to deteriorate rapidly. One key aspect that affects ZIM Integrated Shipping is shipping rates which have not bottomed yet. Continually falling freight rates are set to keep the pressure up on the company’s top line as well as other key metrics.

Final thoughts

ZIM Integrated Shipping reported decent results for the fourth-quarter regarding EBITDA and free cash flow yesterday, but shareholders are not only looking at a steep decline in key metrics in FY 2023, but the dividend is also going to come down by a lot. With the fat dividend of FY 2022 gone and operating fundamentals remaining weak, I see no reason to invest in ZIM Integrated Shipping at this time and I continue to believe that the risk profile is highly skewed to the downside!

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.