[ad_1]

Sundry Photography

Thesis

About a month ago, I upgraded SentinelOne (NYSE:S) stock from ‘Sell’ to ‘Buy’, as I argued that the valuation has come down to levels that allow for an attractive risk/ reward thesis. Now, after SentinelOne reported strong Q4 results, and guided for a nearly 50% YoY topline expansion in 2023, I am confident to reiterate my bullish call. In fact, anchored on updated growth assumptions through 2027, I raise my base case target price for SentinelOne stock to $24.96/share.

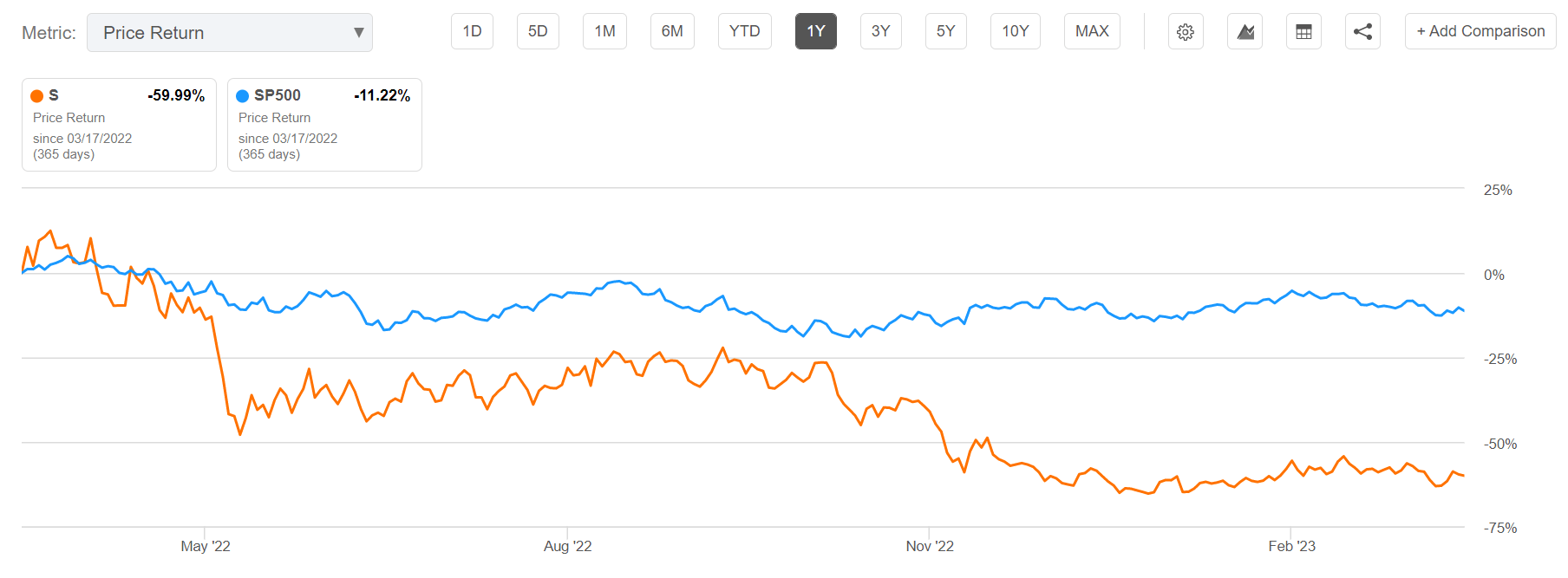

For reference, SentinelOne stock is down approximately 60% for the past twelve months, as compared to a loss of about 11% for the S&P 500 (SPY).

Seeking Alpha

Strong Q4 FY 2023

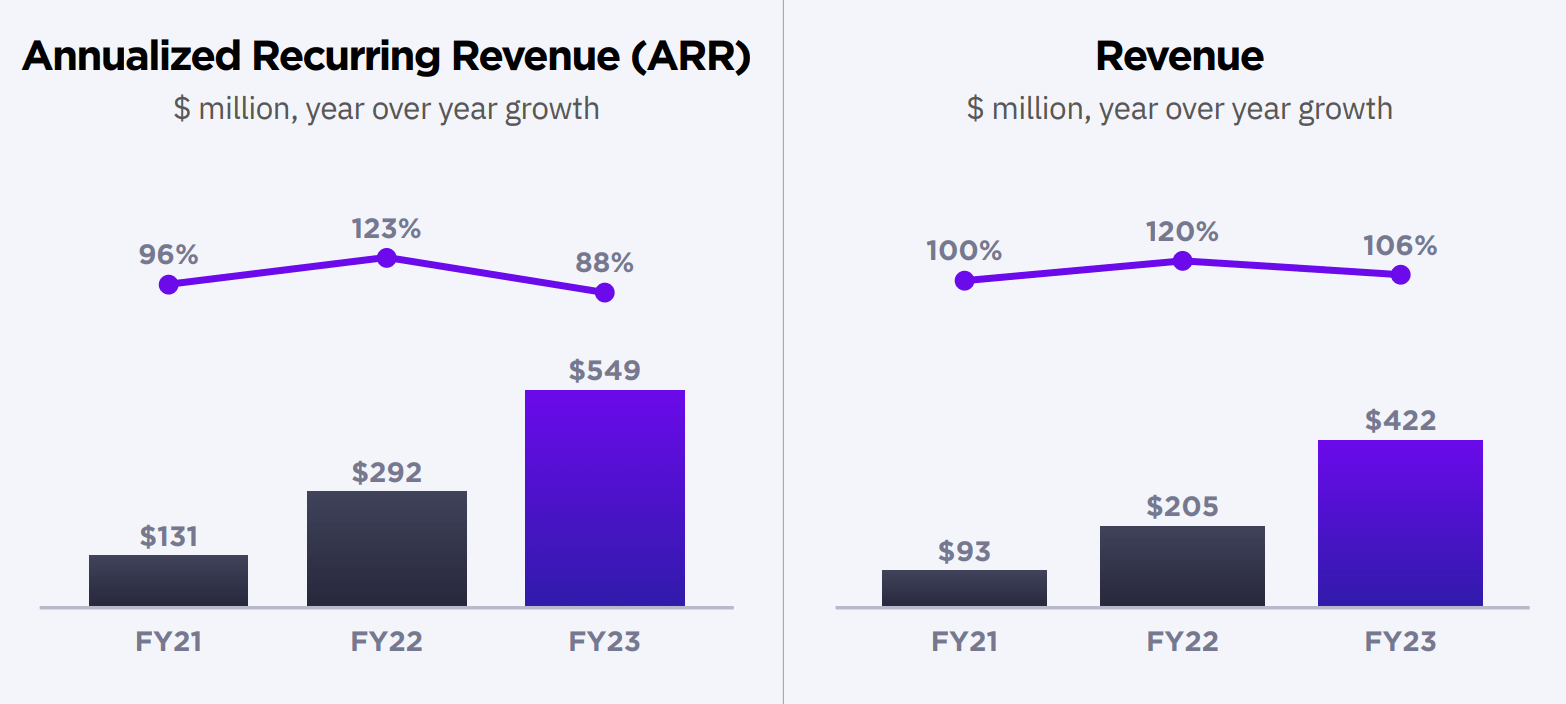

SentinelOne reported strong Q4 results, beating analyst consensus estimates with regards to both sales and earnings. During the period from September to end of December, SentinelOne generated revenues of about $126.1 million, which is almost double the $65.6 million achieved in the same period one year earlier, and about $15 million above analyst consensus estimates (according to data collected by Bloomberg).

SentinelOne’s annualized recurring revenue as of 31 December 2022 amounted to $549 million (88% YoY expansion), while dollar-based net revenue retention rate continued to remain above 130%. Moreover, the company reported that it acquired approximately 750 new customers during the quarter, resulting in a total customer count of over 10,000 at quarter-end (about 50% YoY growth).

SentinelOne Q4 FY 2023 reporting

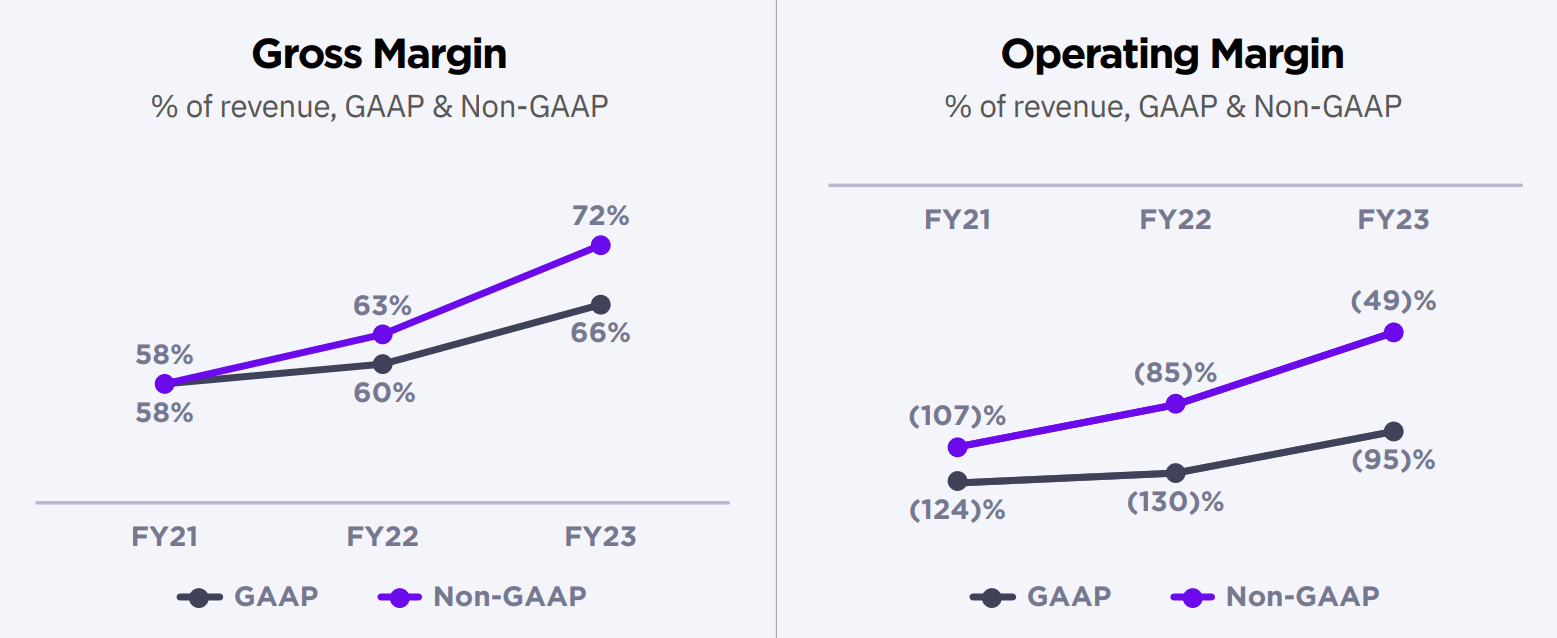

Although SentinelOne continues to write losses, investors should take note that the rate of change for profitability is in the right direction. In Q4 FY 2023, SentinelOne’s GAAP gross margin improved by about 500 basis points, to 66%. Similarly, GAAP operating margin improved to (79)%, as compared to (108)% for the same period one year earlier.

SentinelOne Q4 FY 2023 reporting

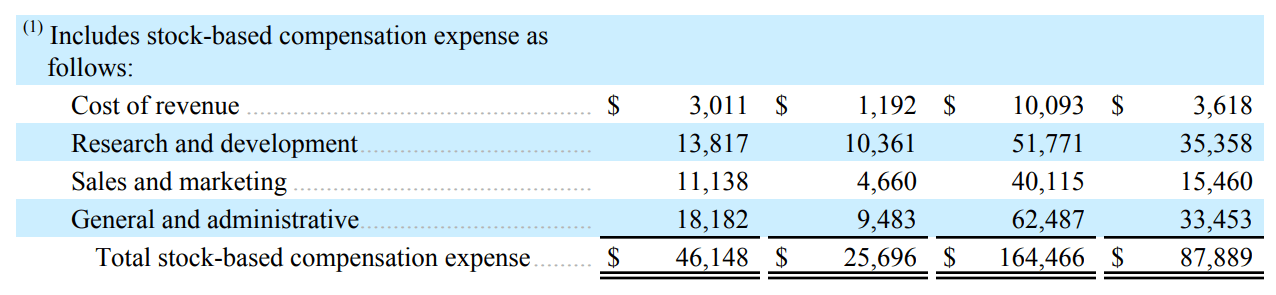

In FY 2023, SentinelOne accumulated GAAP operating losses equal to $403.6 million. Admittedly, there are few periods when such a headline number is not concerning–and especially if the equity and debt markets are kind of frozen. But, reflecting on SentinelOne’s net-cash position of $597 million as of December 31, I am not concerned about the cybersecurity firm’s financial health. Moreover, investors should also consider that about $164.5 million of said losses are non-cash expenses, given that they are attributable to stock-based compensation.

SentinelOne Q4 reporting

Topline Growth Likely To Stay Above 50%

Despite a challenging macro-economic backdrop that might lead to longer sales cycles as compared to base-line, something that management expects to persist in FY 2024, SentinelOne guided for strong growth and improving profitability.

According to management estimates, FY 2024 topline growth could surpass 50%, with revenues growing to between $631 million to $640 million. And as management sees ‘increasing scale, improving data processing efficiencies, as well as expanding our modules’, FY 2023 gross profit margin and operating income margin are expected to improve to about 74% and (27)% respectively (both are mid-point references).

As a sustainable long-term estimate, management continues to see a 20% EBIT margin as achievable.

SentinelOne Q4 reporting

Valuation Update

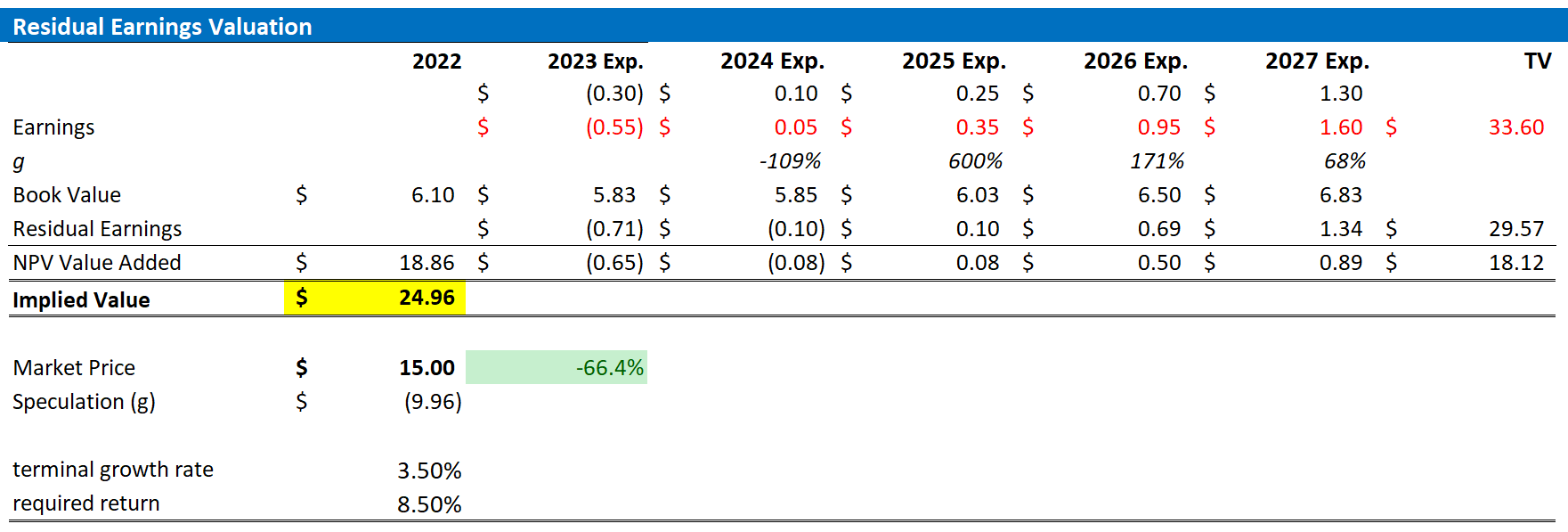

Anchored on stronger than expected growth, I update my valuation model for SentinelOne: As compared to my pre-Q4 assumptions, I now see stronger growth through 2027, but also lower earnings in 2023 and 2024 (due to growth investments such as R&D and Sales expenses). With that frame of reference, I now estimate that SentinelOne’s EPS in 2023 will likely fall to somewhere between $-0.6 and $-0.5, while I raise my EPS for 2024, 2026 and 2027 to $0.35, $0.95 and $1.6 respectively.

I continue to see a 3.5% terminal growth as justified (about one percentage point higher than estimated nominal global GDP growth). And I continue to anchor on an 8.5% cost of capital.

Given the model updates as highlighted below, I now calculate a fair implied share price of $24.96, as compared to $21.01 prior.

(Topline numbers highlight my pre-Q4 2022 assumptions)

Author’s EPS Estimates and Calculations

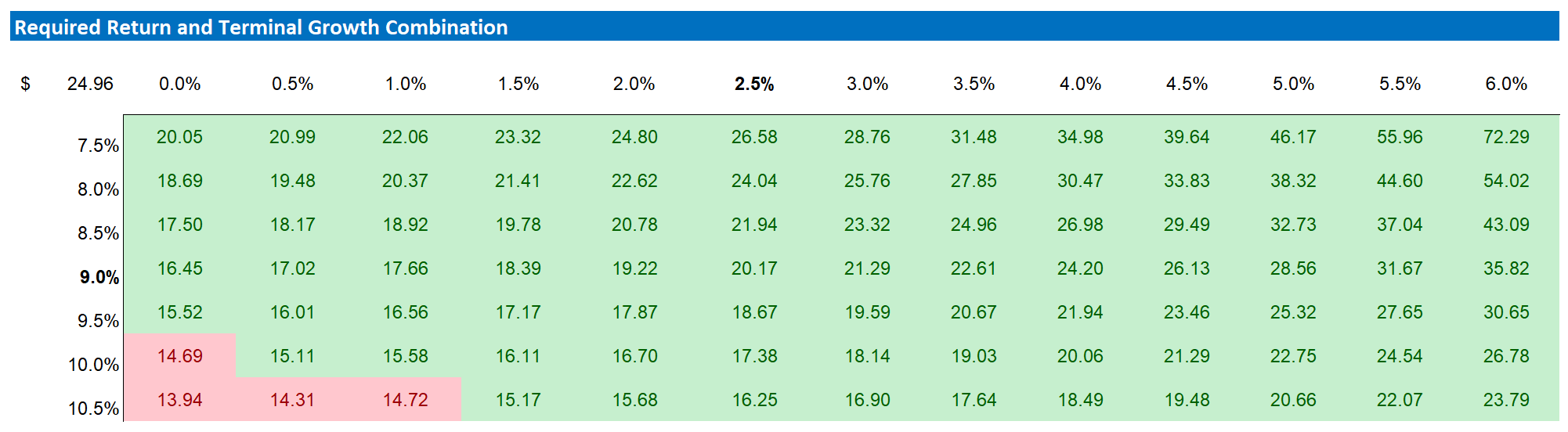

Below is also the updated sensitivity table.

Author’s EPS Estimates and Calculations

Risks

As I see it, there has been no major risk-updated since I have last covered SentinelOne stock. Thus, I would like to highlight what I have written before:

Investors looking to buy into SentinelOne’s equity – despite the stock’s valuation premium – should be aware of the following downside risks: First, SentinelOne is writing losses. There is no guarantee that the company will achieve significant profitability in the next few years, if ever. Second, a worsening macro-environment including inflation and supply-chain challenges could negatively impact SentinelOne’s customer base. If challenges turn out to be more severe and/or last longer than expected, the company’s financial outlook should be adjusted accordingly. Third, investors should monitor competitive forces in the cybersecurity industry. If competition increases more than what is modelled by analysts, profitability margins and EPS estimates for SentinelOne must be adjusted accordingly. Fourth, much of SentinelOne’s share price volatility is currently driven by investor sentiment towards risk and growth assets. Thus, investors should expect price volatility even though SentinelOne’s business outlook remains unchanged. Finally, inflation and rising-real yields could add significant headwinds to SentinelOne’s stock price, as the higher discount rates affect the net-present value of long-dated cash-flows.

Conclusion

SentinelOne continues to not only capture a strong growth tailwind (cybersecurity demand), but also to take market share from competitors — as the firm is strengthening its cybersecurity offering across both endpoint and cloud security. Notably, management expects FY 2024 YoY topline growth to surpass 50%, bringing revenue to a level anywhere between $631 million to $640 million.

Assuming that SentinelOne’s revenue could likely expand to close to $3 billion by 2027 (which is reasonable given the market whitespace in cybersecurity), and a sustainable EBIT margin of 20% (according to management guidance), SentinelOne stock looks materially undervalued at an EV/Sales of about x5.

Given updated EPS estimates, a 3.5% terminal YoY growth rate and an 8.5% cost of equity, I now calculate a fair implied share price for SentinelOne stock equal to $24.96/share. Reiterate “Buy” recommendation.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.